22 June 2026, 5 minute read

What about my spouse?

It’s a top question I’m often asked whenever I speak about, and show people, the MHPD:

Source: MaPS MoneyHelper Pensions Dashboard (MHPD) industry demo full journey video (Nov 2025)

Part 1 of this blog and podcast series showed how, from 2027/28, for the first time, you’ll be able to see what total Estimated Retirement Income (ERI) you might get.

But very many people exist as half of a couple and want to consider both of their ERIs together, imagining their future post-work lives as a pair – it’s a lovely feeling.

And, importantly, people worry what income will continue when one of the partners dies.

In this Part 2 of my 3-part blog and podcast series, on the personal nature of pensions adequacy, I show, through my own and my mother-in-law’s stories, how you need an adequate income long after your spouse or partner dies.

The blog is aimed at payroll & pensions professionals, but read it as the consumer you also are.

30 years ago today

Exactly 30 years ago today (22 June 1996), the wonderful ‘Woodie’ (aka Heather Wood) said ‘I do’ at St Mary’s, Greenham, near Newbury in Berkshire.

Sadly, Heather’s dad Jim wasn’t able to walk her down the aisle as he had died three years earlier, a year before Heather and I got together. It’s a great regret for me that I never met him.

Sadly too, less than eight years after she was married, Jim’s only daughter was diagnosed with breast cancer. Heather coped with it magnificently, bringing up our three children so brilliantly – you wouldn’t have known she was unwell at all really. It was inspiring to witness.

But after 10 years, the cancer metastasised to Heather’s bones, and she declined rapidly during 2014, dying on 25 June 2014, three days after our 18th anniversary.

So, on our 30th anniversary today, Heather’s been physically absent for 40% of those last three decades.

But she’s still very present, in lots of ways, not least due to a monthly payment I receive.

Spouses pensions really matter

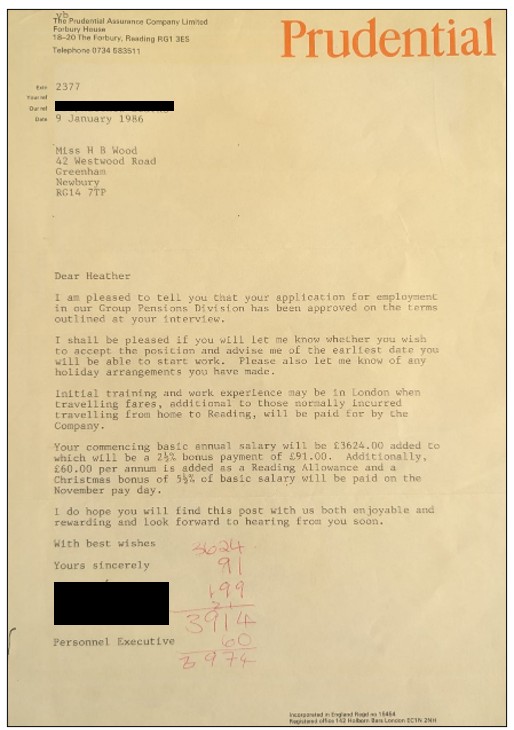

We’d met at the Prudential (or the Pru) in Reading, where Heather had worked since 1986. I joined in 1991.

After she died, I found her offer letter from January 1986:

I love how she’s worked out in red pen that her basic salary, plus annual and Christmas bonuses, and Reading Allowance, are just £26 shy of £4,000 a year. Not bad at all in 1986!

Heather worked hard at the Pru and progressed and, as was standard in those days, was enrolled into the company’s Defined Benefit (DB) pension scheme.

Had dashboards existed in the 80s, alongside her State Pension, she’d have been able to see her ERI from the Prudential Staff Pension Scheme (PSPS), coming into payment from next year (2027) when she would’ve reached the scheme’s normal retirement age of 60.

Dying at age 47, Heather never drew the pension she’d built up. But it didn’t disappear: it survived her.

As her surviving spouse, I am entitled to be paid a monthly PSPS Spouses Pension.

Set up right, pensions survive death. And not only that, they can go up each year too.

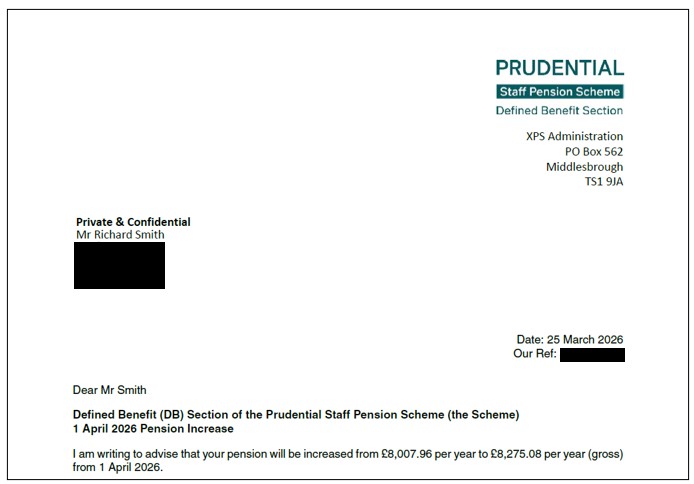

When Heather died in 2014, my starting spouses pension was about £6,000 a year, or £500 a month.

But, over the last 12 years, as you can see from the letter below, it’s increased by a third:

This lifetime ongoing income of £8,000 a year – twice Heather’s starting earnings 40 years ago in 1986! – has been tremendously helpful as I’ve brought up our three kids on my own.

And it’s now a key part of my own retirement planning.

Decades of love

But more than being merely financial, it’s a monthly message of love, spanning decades of time.

Just because Heather accepted an offer of:

- employment from the Pru in 1986, and

- marriage from me in 1996,

I will benefit for the rest of my life, potentially until the 2050s.

But my 12 years to date of being a spouse pensioner is dwarfed by my Mother-in-Law Marion. Heather’s dad worked for the BBC, so Marion has now been a recipient of a spouses pension from the BBC Pension Scheme for 33 years. Decades of ongoing love.

This is the adequacy truth often missed: your future stability can depend on decisions someone else made decades before you ever needed them.

Dashboards – a window across decades

It’s really important to think of pensions adequacy of your whole household, even after you’ve gone. This doesn’t always happen. Despite death being a certainty, the Second Pensions Commission’s Interim Report highlights (on page 172, paragraph 5.102, if you’re interested):

“Planning for this eventuality [i.e. death of one of the partners] is typically fairly limited”.

I hope pensions dashboards will help change this.

What dashboards make visible is the fact that pensions are about the long term, spanning many decades.

I discussed this notion with Claire and Chris Sandys on their lovely podcast, The Silent Why.

The episode (Loss #64 of 101 different types of loss Claire and Chris are covering) was actually recorded exactly a year ago, on Heather’s 11th deathiversary, but it’s all still very true, one more year on.

Dashboards present a window to your life: showing pensions you built up from your various jobs decades ago, which will pay out as retirement income to you, or to your surviving spouse, decades into the future.

Decades of work, and life, and love, right there on your phone.

My experience of becoming a pensioner at the age of 46 has crystallised this emotion for me.

It’s partly why I’m so passionate about dashboards.

The passion also comes from missing Heather, which of course the kids and I still do every day.

As I said to Claire and Chris, it’s “no surprise that the word passion has got pain running right through it”.

For me, trying in some small way to help millions of UK citizens get the benefit of a pensions dashboard is a way of giving my grief some purpose.

Summary

Part 1 showed how pensions adequacy is a relationship: between your unique past to date and the choices you make today for your future.

I’d now expand that: yes it’s about your choices, but it’s also about dealing with what just happens to you. Heather didn’t choose her diagnosis, it just happened.

None of us know the future, but that doesn’t mean we shouldn’t try to plan for it.

So in 2027/28, as you sit next to your spouse or partner on the sofa, both logged in to the dashboard, looking at your respective total ERIs on your phones together, ask yourselves:

“If I go first, how much of the total ERI I’m seeing will continue for her / him? And how much will be enough for them on their own?”

(Maybe think about the ERICA idea, but with changed spending needs for a single household.)

Thinking like this, together, is possibly your greatest long-term act of love.

Don’t be scared to think about death, it’s certain, so not to be feared. As Khalil Gibran said, who I quoted on The Silent Why: “Our anxiety does not come from thinking about the future, but from wanting to control it”.

Prepare for it as best you can, then relax and enjoy the day, whilst loved ones are still here with you.

A final little P.S. Thinking of our Pearl anniversary and where pearls come from, I’ve found a lovely charity in Scotland, where Heather was born, which I’ll make a donation to as a 30th anniversary present to her – it’s called Seawilding, the UK’s first community-based native oyster and seagrass restoration project.

In the final Part 3, in August, I’ll look at one way to prepare for the future: thinking about how you’re choosing to spread your spending consumption across the whole of your life.

Thanks so much for reading right to the end x

RS 22.6.26