Introduction

The Belgian pensions dashboard is mypension.be.

On 12 June 2023, I had the absolute privilege of visiting the mypension.be team in Brussels at the very start of my Pensions REDUX tour.

The core purpose of the tour was to learn more about mature pensions dashboards’ user experiences (UXs) and user interfaces (UIs).

So the main findings below focus on the high-level UX and UI before, whilst, and after using mypension.be.

The Belgian team were also very generous providing me with other insights, such as usage statistics, so I’ve included some of these findings below too.

Before reading on, for context please do have a look at the Background and 10 General Comments page.

After reading the findings below, feel free to get in touch with me if you’d like to talk about dashboards, discuss the findings, and what they might mean for forthcoming pensions dashboards in the UK.

What’s on this page?

Other information about mypension

UX before using mypension

mypension.be is an online service well-known to Belgians. It is a government funded service and it has one of the biggest brand recognition rates of all Belgian government services.

Across the population, it is Belgians’ preferred source for finding out information about their pensions.

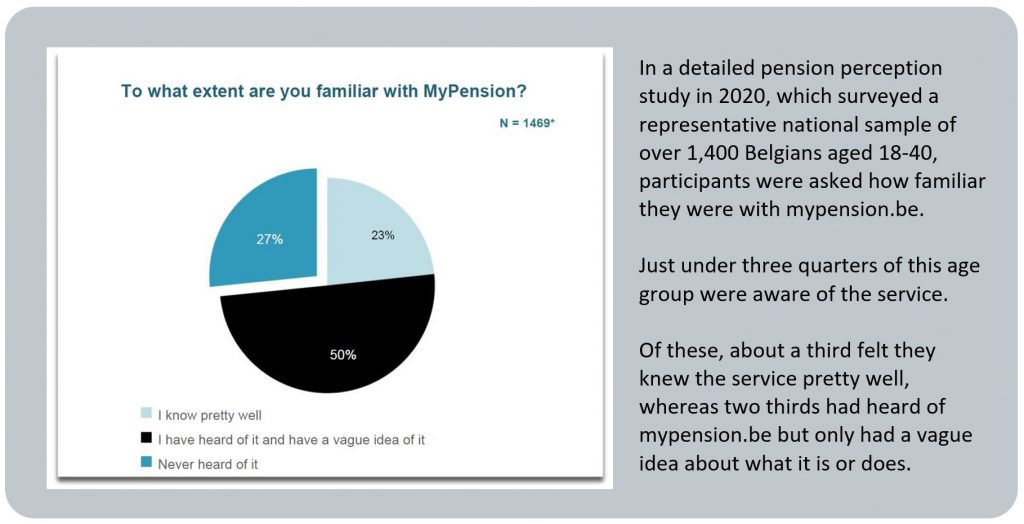

Pensions dashboards tend to be most used by people later in their careers, i.e. as they approach the age they might want to stop, or reduce, work. But what about awareness of mypension in younger people?:

BLANK

Every autumn a “push” communication is sent out alerting those Belgian citizens who are actively building up a Pillar 2 pension that pension data has been updated. This communication promotes the mypension brand (as do all communications from the mypension team) and results in a usage spike in December each year (see Usage of mypension below).

In addition, the brand is also promoted by other stakeholders, such as Belgian politicians and media, sometimes generating spikes in usage of mypension, and sometimes with wonderful Belgian humour:

BLANK

Arriving at the dashboard, users can choose whether to see the service in Dutch, French or German (because of the different language speakers in Belgium). An English version is also in the pipeline.

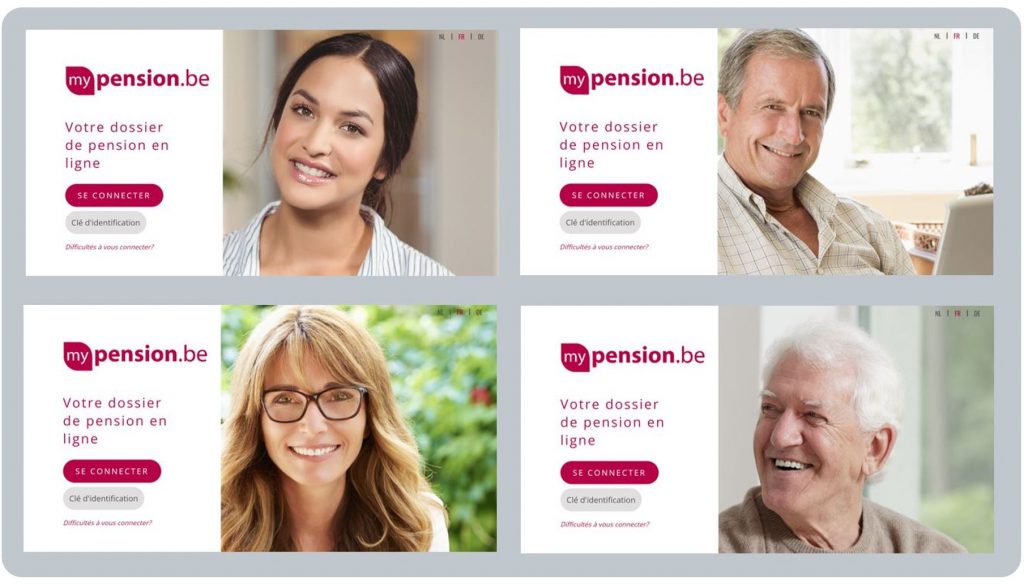

The desktop browser version has a carousel of different people images on the homepage of mypension.be (if you’re reading this on a desktop browser right now, why not click the link and see who comes up):

BLANK

These four personas are used consistently in the marketing of mypension.be:

The persona-specific questions on the four posters above are:

- Charlotte, age 32: “What will my pension be if I stay in my current role?”

BLANK - Sabine, age 42: “I have a clear view of how my supplementary pension is building up”

BLANK - Marc, age 57: “Working less or getting a bigger pension? Thanks to mypension I was able to make the right choice”

BLANK - Roger, age 73: “My pension payments are announced a few days in advance”

The four personas were created to make users feel welcome and that the service is of relevance to them (whatever life stage they are at). mypension’s core functionality has been designed to support the key requirements of these different users, namely:

- overview of pension in ‘build up’ phase, i.e. through working life

- information on pension impacts of different work and life event, e.g. changing jobs, marriage, etc.

- process for claiming your pension, i.e. at retirement.

[Note that mypension also supports retired Belgians, but I’m not covering this here as it’s not relevant to the UK’s initial dashboards, which will only be for people with pensions in the working life ‘build up’ phase.]

BLANK

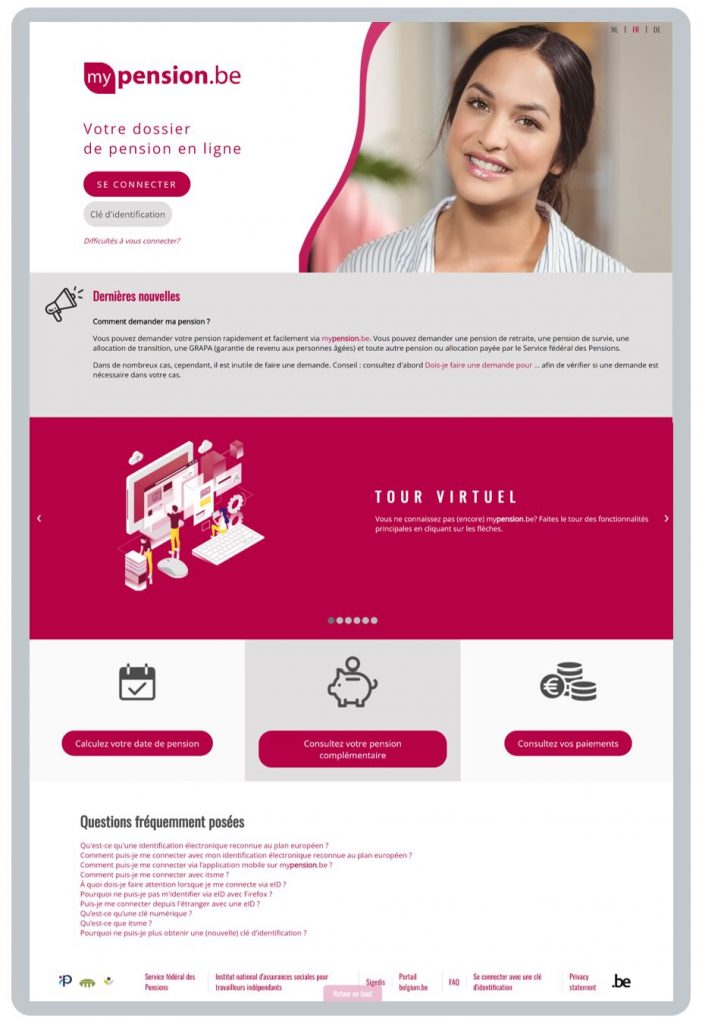

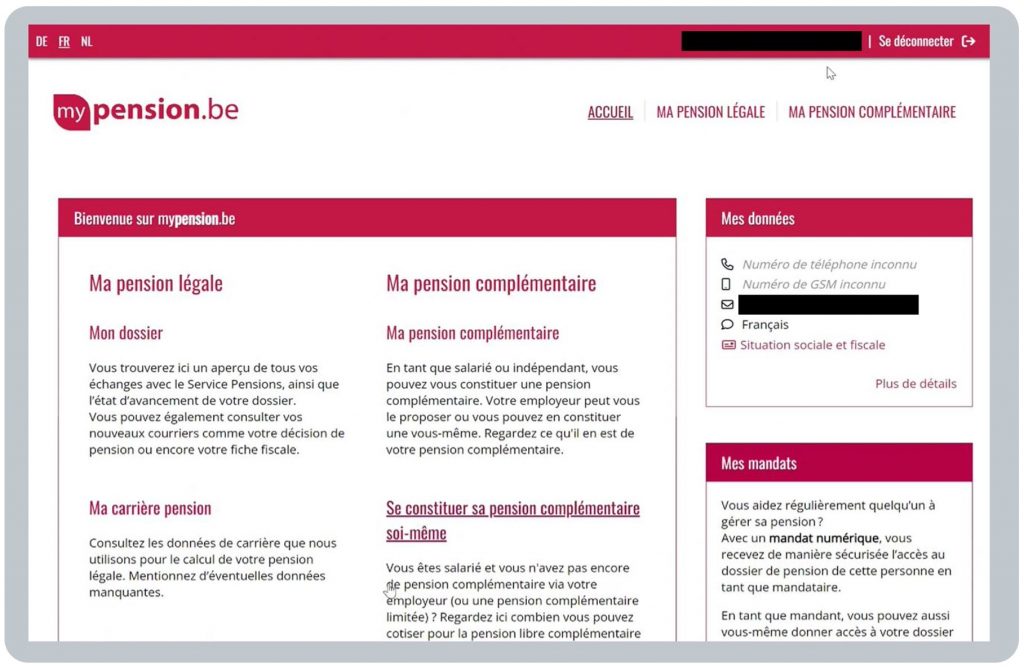

What can you see before logging in?

The mypension.be homepage includes:

- a virtual tour, describing the main functionality of mypension – you can:

- investigate your pension payments (for those already in retirement)

- review your messages / correspondence with pension institutions

- calculate and plan when you can take your pension (for those not yet retired)

- find out about your supplementary pension (i.e. Pillar 2)

BLANK

- some FAQs (which, on the homepage, are mainly about logging in to mypension)

BLANK - links to the three organisations who collaborate to operate mypension.

BLANK

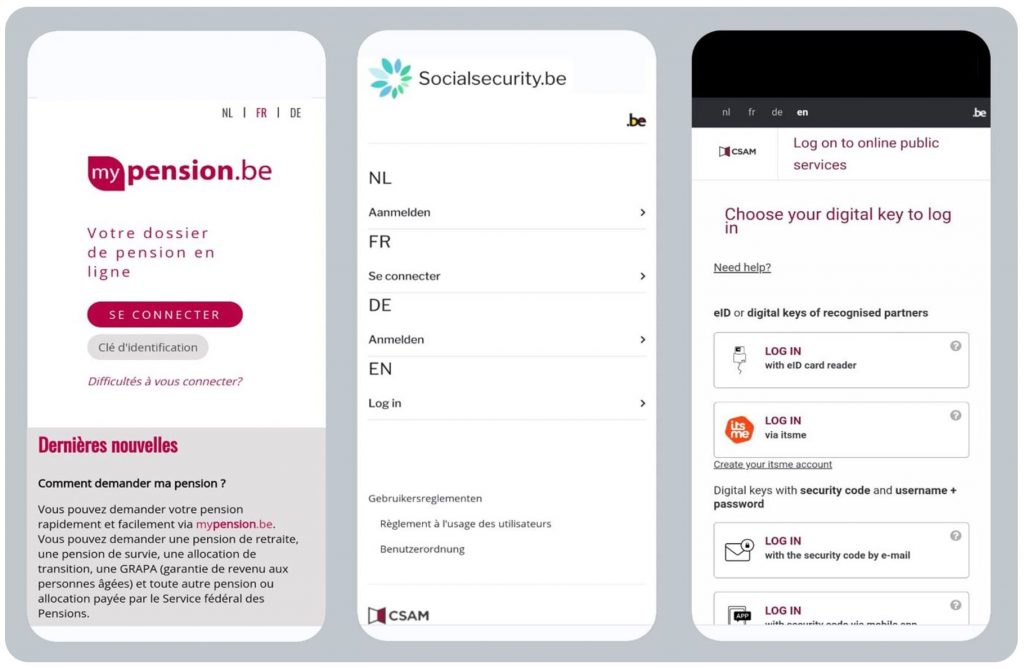

On the homepage, users are invited to click “se connecter” (log in), and then asked to choose their digital authentication route (a central Belgian Government service not managed by the mypension team):

All Belgian citizens have an eID so in theory the service is available to everyone. As explained in General Comment 5, there’s not much point covering Belgium’s central digital identity service in any detail here – it is what it is, and the UK’s identity service will be what it will be, i.e. there are no design choices to be made here by UK dashboard operators as they will all be required to use the same central identity service.

Data matching of citizens to their pensions is achieved by using each Belgian’s National Registration Number (NRN), which is verified by the central Belgian Government authorities. In the early days, a lot of work had to be done to ensure all pension schemes and providers held a correct NRN for all their members. This was done through checking other personal details, which uncovered issues with items such as variable First Name spelling and partial Dates of Birth.

This upfront work was critical to ensure matching worked correctly when mypension was launched and was really important because a solid “back end” data is essential for a good “front end” user experience.

BLANK

BLANK

UX whilst using mypension

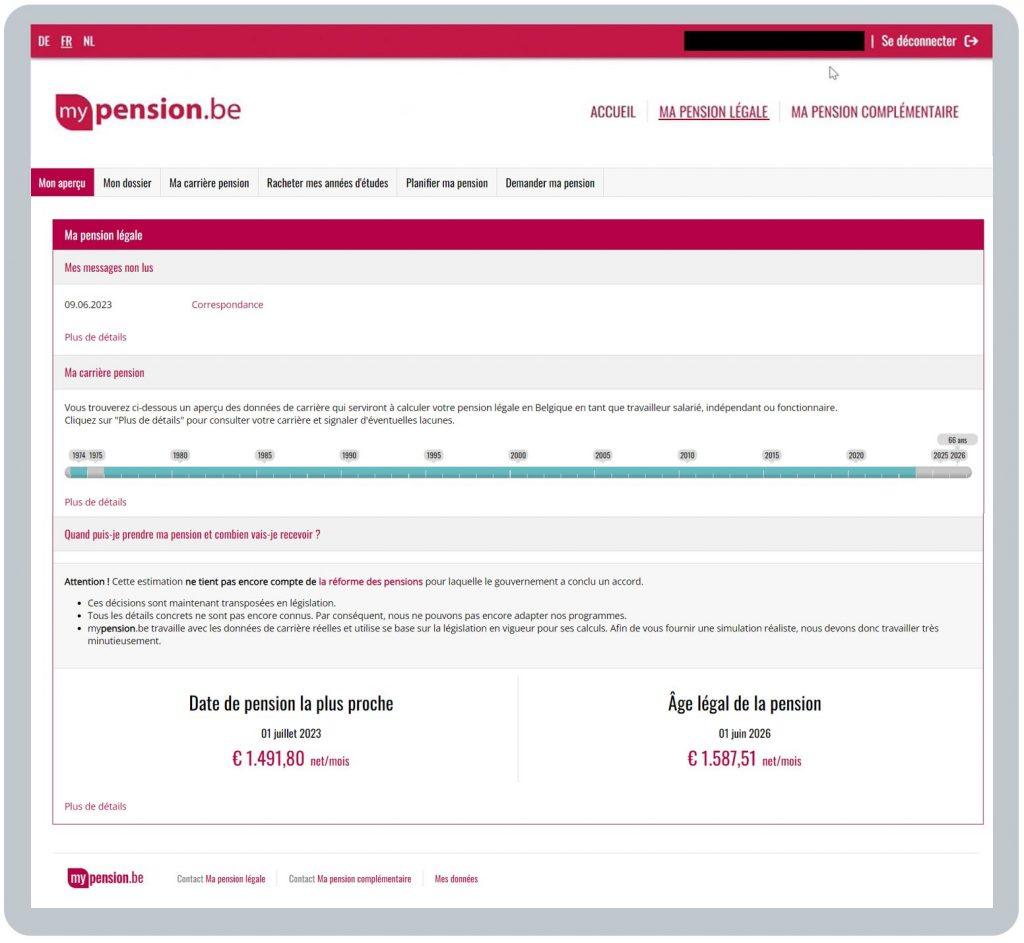

Once logged in, the user sees the landing (or welcome) page of mypension (the user’s name and email address in the example below have been redacted for privacy):

This page immediately shows the user the two core elements of their total pension:

- Ma pension légale (“My statutory pension”): this is the Pillar 1 state pension

- Ma pension complémentaire (“My supplementary pension”): this is Pillar 2 on top

The pension structure is quite specific to Belgium, so I won’t cover it in detail here (see General Comment 3), except to highlight that, for many Belgians, their Pillar 1 pension makes up the majority of their retirement income. Pillar 2 pensions are widespread but are generally relatively small in relation to Pillar 1 pension incomes. The website pensionstat.be contains many useful statistics on this and other topics.

Clicking on Ma pension légale or Ma pension complémentaire takes the user to two different online services, i.e. a total pension picture isn’t shown.

Pillar 2 pension is nearly always taken as a cash lump sum which makes it problematical to display Pillar 1 and Pillar 2 pension incomes together as a total pension income. However, new rules coming into force make this simpler, and it’s on mypension’s development roadmap for future years to show a total income.

Below is a summary of what a user sees in the Pension légale and Pension complémentaire areas.

BLANK

Pension légale

On the main pension légale page the key things a user sees, working from the bottom upwards, include:

- net monthly income it’s estimated the user might get from the date they attain state pension age (bottom right) (in this example €1,588 a month after tax – at current exchange rates, that’s about £1,360 a month net)

BLANK - reduced net monthly income it’s estimated the user could get from the earliest date from which it can be taken (bottom left) (in this example €1,492 a month after tax, or about £1,280 a month net)

BLANK - caveat that the income calculation estimates shown are only based on current data and legislation

BLANK - career history timeline showing, in blue, the working life years contributing to the pension légale

BLANK - important messages from mypension

BLANK - menu options along the top offering the user a lot more detailed information on their career timeline, redeeming years when they were studying, calculating the pension impacts of various changes (such as working part-time), and how to claim Pillar 1 pension to bring it into payment.

BLANK

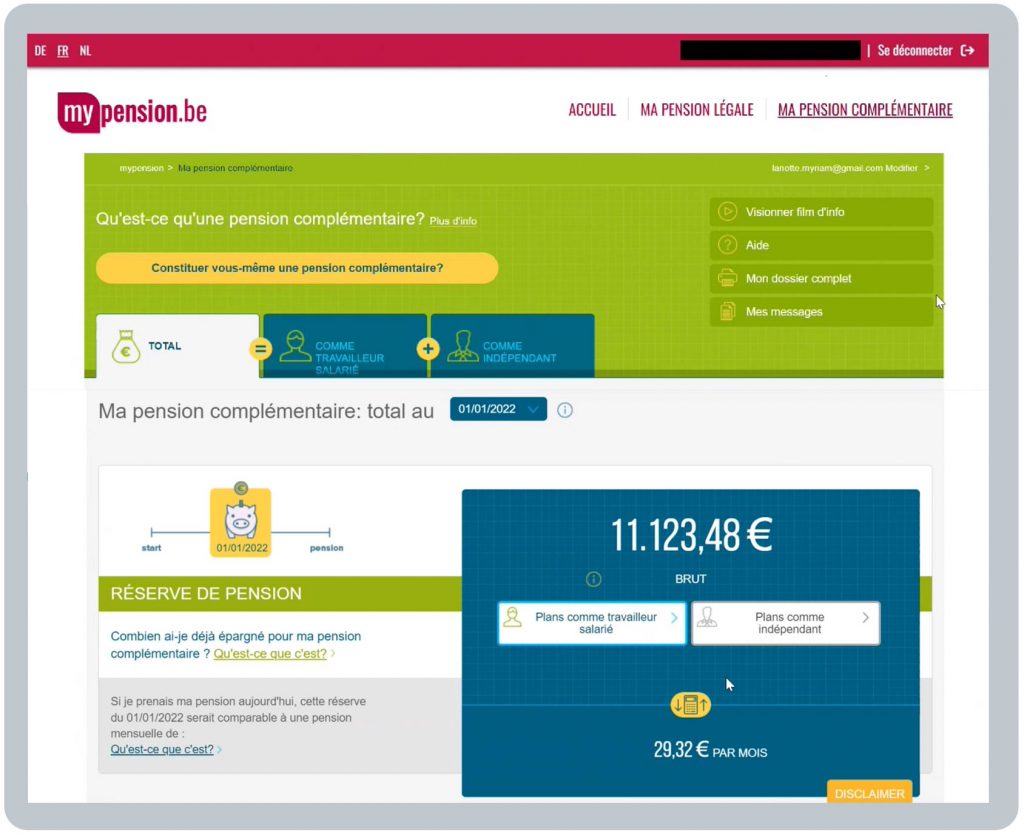

Pension complémentaire

As you can see, the Pillar 2 (pension complémentaire) display has a very different look and feel to Pillar 1 (pension légale), but it is accessed through the same single sign-on.

On the pension complémentaire page the key things a user sees, again working from the bottom upwards, include:

- notional gross (brut) monthly income the Pillar 2 fund / reserves might provide in retirement (if it’s taken as an income and not a lump sum) (bottom right) (in this example €29 a month gross, at 1 January 2022, but users have fed back they’d like to see this net, i.e. after tax)

BLANK - total DC pension fund (or DB “vested reserves”) (in the example above, the fund is €11,123)

BLANK - history of pension fund values at previous annual dates (drop down list next to 01/01/2022)

BLANK - numerous options to view more details about the pension complémentaire, including a projection of what the value of the fund could be in the future (which isn’t highly used), and an option to download your data to a pdf (which is highly used)

BLANK - various help information including a short video explaining more about pensions complémentaires and information on how to contact your different pension providers.

BLANK

BLANK

UX after using mypension

Many users’ core interest in their overall pension position can be boiled down to three simple questions:

- What have I got?

- Is it enough for me to live on in retirement?

- What can I do?

In Belgium, the core focus of mypension.be is to help Belgians answer question 1.

Users can see clearly what Pillar 1 pension income (pension légale) they may get in retirement, as well as any additional Pillar 2 pension (pension complémentaire) they may have on top of Pillar 1.

mypension also allows users to download and print their Pillar 2 pension information (Mon dossier complet) for future reference if they wish (with plans to broaden this to both Pillars in the future):

BLANK

mypension.be is focused on providing neutral, unbiased, non-commercial, and trustworthy information provided by the Government.

So, in terms of the second two questions (“Is it enough?” and “What can I do?”), mypension lets users address these more subjective questions themselves afterwards.

For example, after using mypension, Belgian citizens may take steps to:

- understand what pension income they may need in retirement (there’s a generally accepted consensus in Belgium that, on average, people should strive to have an income in retirement which is around 70% of their income prior to retiring)

- learn more about pensions generally to give wider context

- speak with an adviser or others who can help on pensions

- take appropriate steps to improve their pension position if they wish to do so.

BLANK

Taking action

As discussed in General Comment 7, the extent to which users actually make changes to their pension position after using mypension.be is not explicitly visible to the mypension.be team.

This is because mypension deliberately focuses on offering an impartial “Find and View” service which primarily seeks to empower consumers, helping them to feel more confident and better informed so they are able to make better decisions if they wish.

BLANK

BLANK

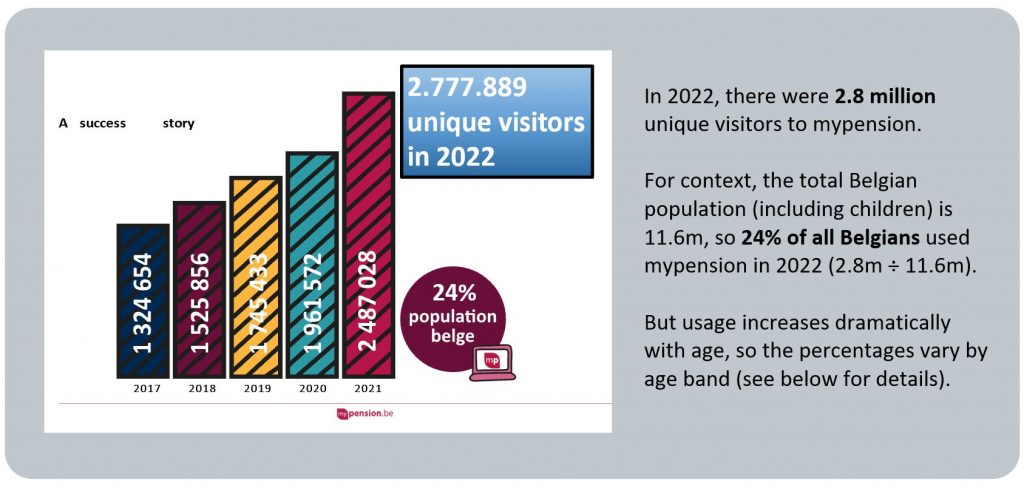

Usage of mypension

The number of unique visitors to mypension.be has been steadily increasing over recent years:

BLANK

The 2.8 million unique visitors to mypension.be in 2022 visited the site just over 10 million times in 2022.

Younger users tend to visit just once a year, but older users approaching retirement visit it many times.

On average, across all age groups, users visit mypension.be between three and four times a year.

(Users might also visit several times in one day, but that’s not counted in the 10 million total visits figure.)

BLANK

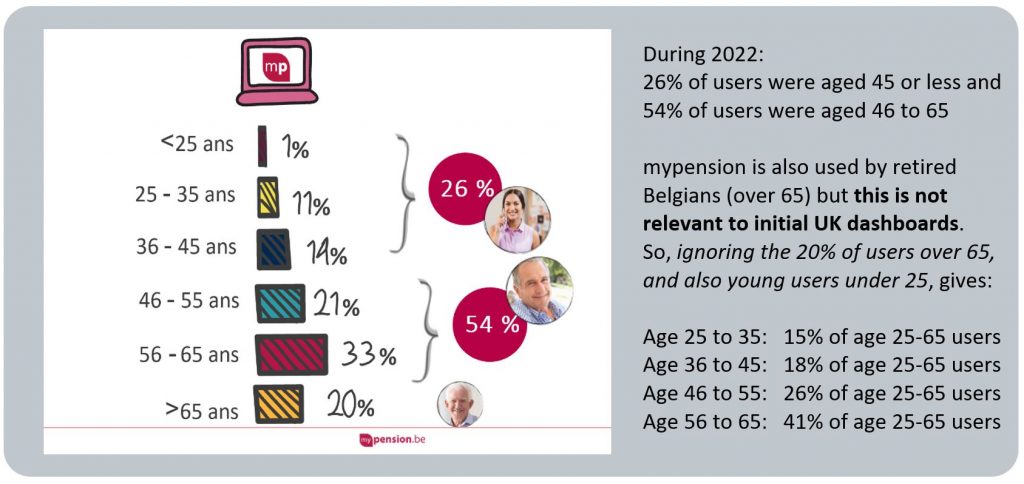

Usage by age

The majority of mypension users are in older age bands:

So, as a crude rule of thumb, focusing solely on the core working age Belgian population, aged 25 to 65, you could say that, roughly, mypension.be users are split:

- one third: under 45 (i.e. 15% + 18%), and

- two thirds: 45 or older (i.e. 26% + 41%).

BLANK

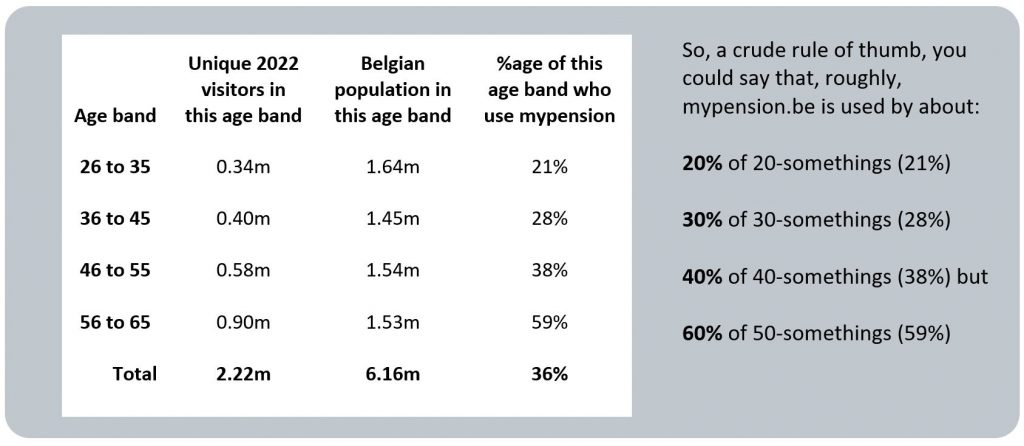

So a higher proportion of each Belgian age band are mypension.be users. Thinking again solely about the core working age population from age 25 to 65, here are the usage percentages by age band:

BLANK

Usage by gender

Slightly, but only slightly, more males than females use mypension.be with a 53% male / 47% female split.

BLANK

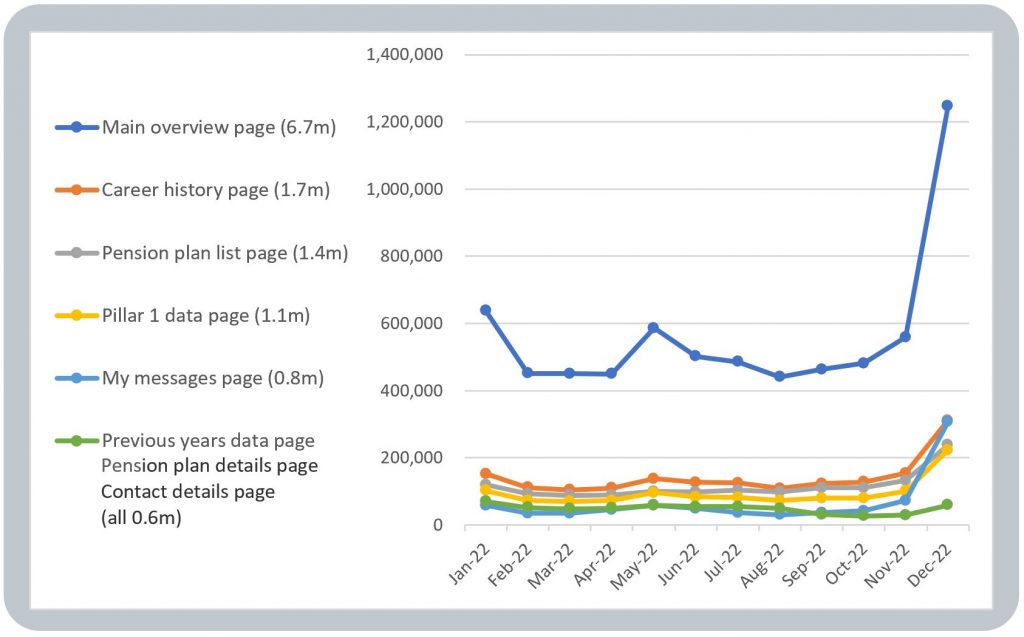

Most visited pages

Most people just want to see their pension overview, and this increases in December each year following an autumn “push” communication (see UX before using mypension above).

The graph below lists the most visited pages / features of the Pillar 1 area of mypension.be – these are the eight pages which were visited over half a million times during 2022).

The graph shows both the total number of page visits in 2022 and the variation from month to month:

For example, the Main overview page was visited 6.7 million times during 2022 (by the 2.8 million unique users), but 1.25 million of those 6.7 million page visits took place during December 2022 (see the spike in the blue line).

A relatively small number of users (typically Type B users – see General Comment 2) do use the more detailed pages, and a lot of effort can be required to develop rich functionality for this type of user.

Steven Janssen, one of the mypension team who I met in Brussels, estimated that:

“90% of dashboard development effort can be for 5% of users (or 10% at the most)”.

BLANK

Different device usage

In terms of the different devices which people use to access mypension.be, mobile devices tend to be used more when people are just looking for an overview of their pension (for example the Main overview page).

Mobiles tend to be used more when people are starting their engagement with mypension.be, perhaps at younger ages, and when they just want to have a quick look, rather than getting into a lot of detail.

However, when people want to investigate and think about their pensions in more detail (for example, on the other key pages shown on the graph above), and certainly when they come to make decisions and take action, then users tend to access mypension.be on laptop / desktop browsers.

BLANK

BLANK

Other information about mypension

The core purpose of my research tour in June 2023 was to learn more about mature pensions dashboards’ user experiences (UXs) and user interfaces (UIs). However, the Belgian team were also very generous providing me with various other insights about the Belgian dashboard, which I’ve summarised below.

This “Other information” section covers some summary points on the:

- history of mypension

- governance of mypension

- vision for mypension.

BLANK

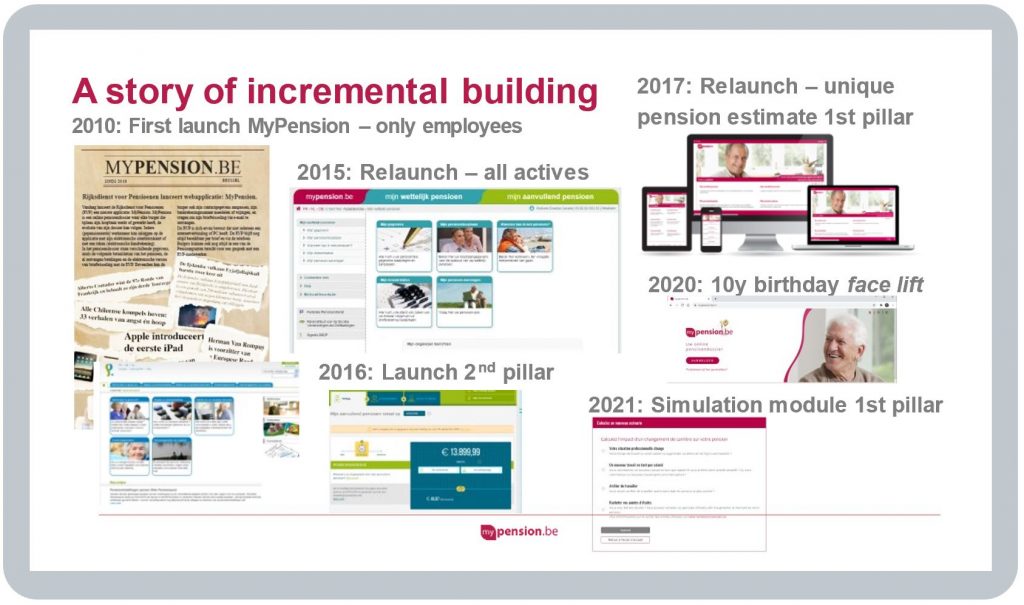

History of mypension

mypension.be was launched in 2010 building on the success of a previous website kenuwpensioen.be (knowyourpension). But mypension.be wasn’t conceived as a stand-alone service, rather it was built on pre-existing databases, collected for other purposes, covering Belgian:

- employment data (necessary for calculating Pillar 1 pensions) and viewable via mycareer.be, and

- occupational pensions data.

A second key element in the creation of mypension was the evolution towards a highly digitised workflow management back-end system for Pillar 1, requiring an equally digitised way of interacting with citizens.

These two elements made the mypension.be information portal both possible and necessary. Since then, from its launch in 2010, mypension.be has been further developed considerably over the years. For example, the 2017 relaunch focused on the mypension UX across desktop, laptop, tablet & mobile devices:

mypension’s 10th anniversary was celebrated in a November 2020 news article containing more history.

BLANK

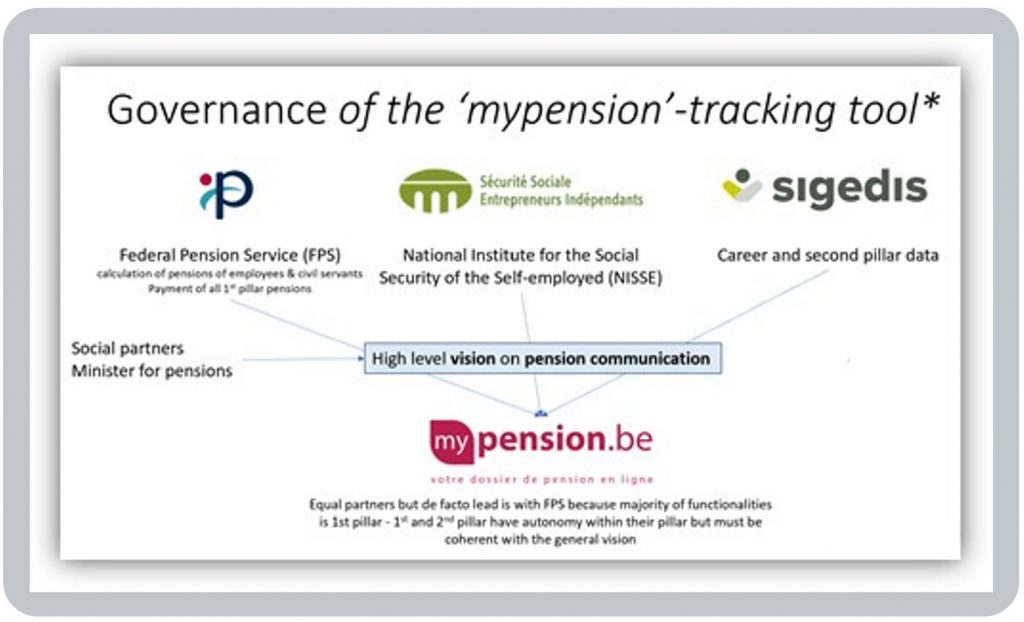

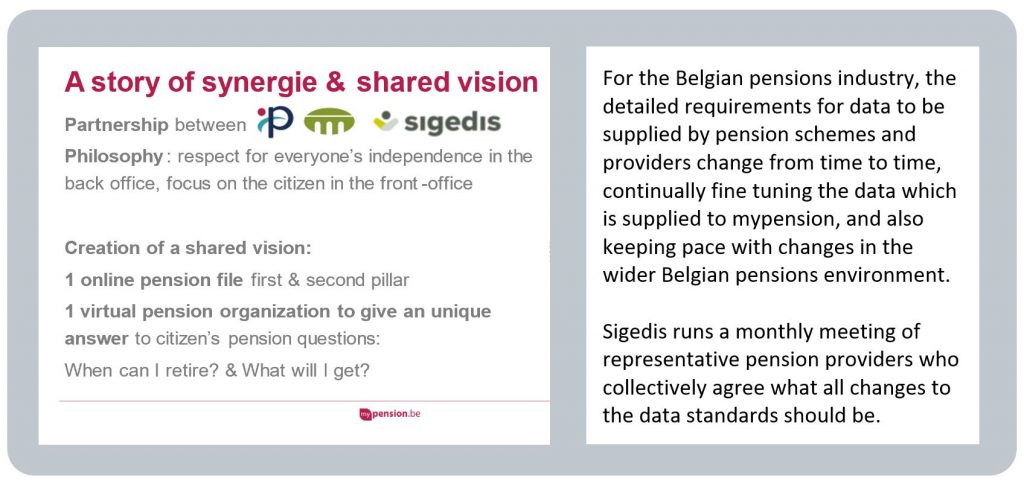

Governance of mypension

mypension is co-managed by:

- Belgium’s Federal Pension Service (FPS)

- the National Institute for the Social Security of the Self-employed (NISSE) and

- Sigedis, a non-profit public body (funded by the Belgian Government) specialising in individual social data.

BLANK

Vision for mypension

A core purpose of mypension.be is to be there when a Belgian citizen needs it, giving reassurance that, even if you haven’t personally kept track of your pensions over the years, there is a central, trustworthy place you can go to and find out about your total pension position. So awareness of the service is key.

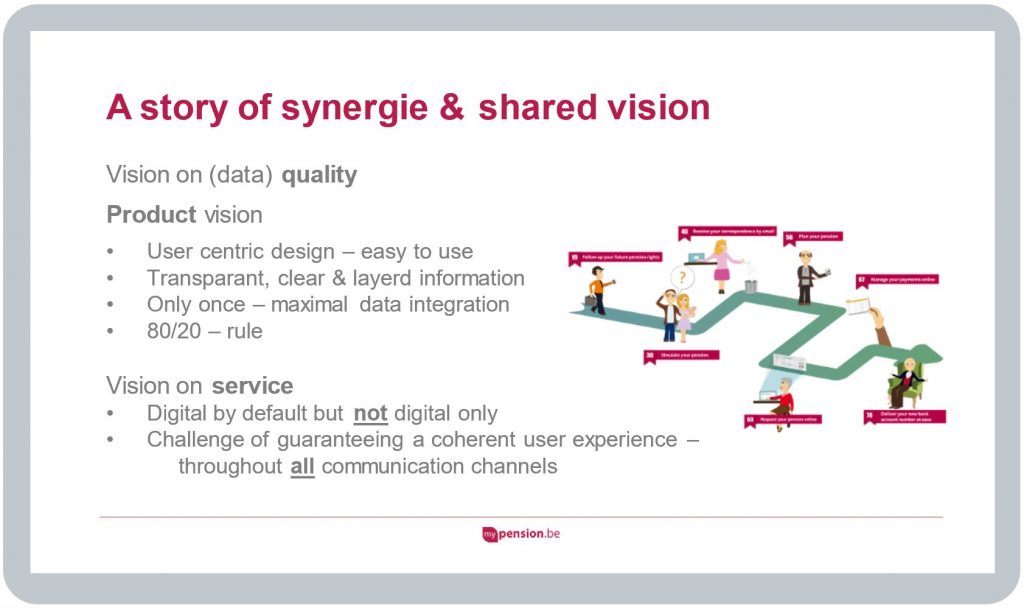

The shared FPS / NISSE / Sigedis vision for mypension, in terms of both product and service, is:

User centric design which is easy to use means simplicity i.e. as little text as possible and very straightforward and easy to use navigation within the dashboard.

The 80/20 rule above refers to a principle of aiming to deliver a core pensions dashboard which is useful and relevant for the majority of users, without spending undue effort on less common situations and issues which only benefit a relatively small minority of users.

Overall, the core thing mypension.be does is build confidence and trust in pensions.

As Steven Janssen said, quoted in my LinkedIn post straight after I met the Belgian team:

“The cost of doing pensions dashboards is cheap for the great deal of trust in pensions they create – dashboards are just the right thing to do”.

BLANK

BLANK

Page content verified by the mypension.be team on 23 September 2023