Who am I?

Hello. My name is Richard Smith.

I’m a career pensions professional, starting in 1987 (see my LinkedIn profile for details).

It was an absolute privilege during 2020 to lead the UK Government’s development of data standards for pensions dashboards (originally published in December 2020), and then to subsequently support PASA and PLSA (now Pensions UK), as well as PensionFusion and Moneyhub on the topic of pensions dashboards.

During 2024, I was also the Volunteer Chair of the (Pensions) Dashboard Operators Coalition, and in 2025, I’m full time pro bono publico on dashboards.

Why I’m a supporter of pensions dashboards

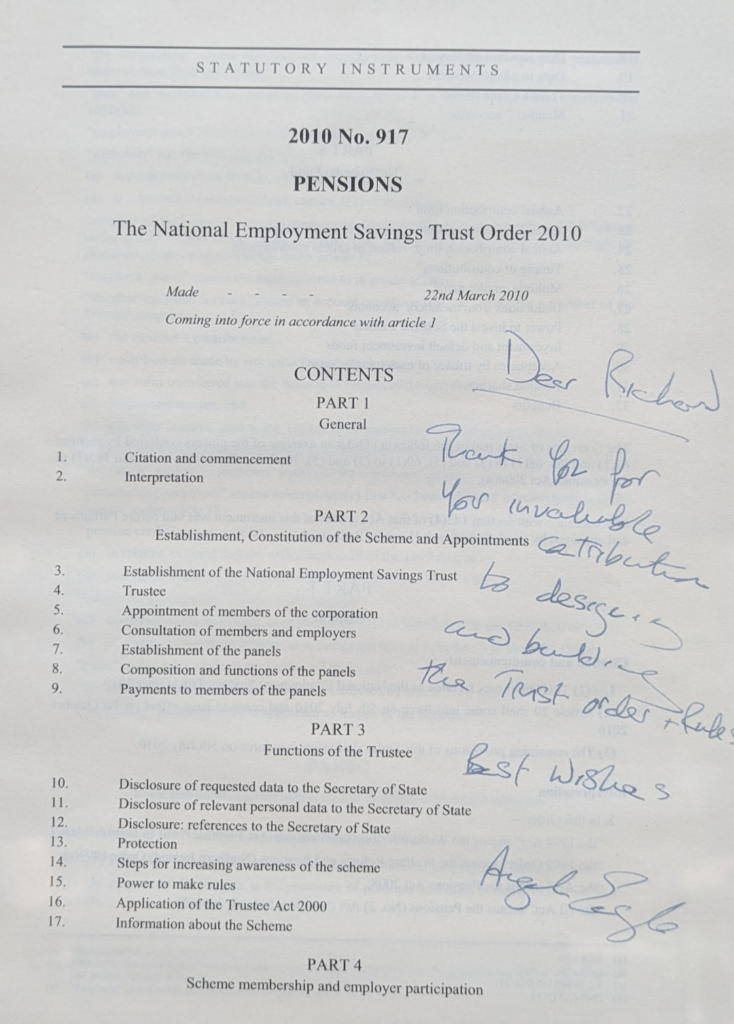

From 2007-10, I was privileged to help the Department for Work and Pensions (DWP), and then the Personal Accounts Delivery Authority (PADA), with the set up of Automatic Enrolment (AE) and the National Employment Savings Trust (Nest) Order and Rules.

The consumer insight research coming in to inform NEST’s design really helped me understand how confusing and worrying most of the UK population finds the topic of preparing for retirement, and thinking about the future and money generally.

It would be great if people could feel much more confident about their prospects for later life, but without having to actively engage or understand a great deal.

Confidence would help people stop worrying so much about whether they’re saving enough for a comfortable retirement, and when (or even whether) they’ll be able to retire.

Confidence comes from information and knowledge. In particular, being able to see in one place all the pension income you’ve built up so far in your career to date. This is just what pensions dashboards are for.

Moreover, I believe the whole arena of pensions for consumers in the UK will be much improved by pensions dashboards, because of the greater confidence they will bring.

Why I’ve set up dashboardideas.co.uk

Like many others in the UK, I’m a supporter of the concept of pensions dashboards, but not at any price.

The complexity and fragmented nature of the UK pensions system is going to make it very hard, and potentially quite expensive, to develop comprehensive dashboard services.

In 2002, the Government previously tried to develop an Online Retirement Planner with a similar focus, but the project was scrapped in 2006 after four years’ development.

The 2017 industry prototype and the 2018 DWP consultation brought up lots of options, each with different pros and cons, requiring extensive discussion and debate. Government has now settled many of these options, and we’re now well into delivery mode, working collaboratively between industry and Government.

By clearly airing and illustrating key issues (for example on my Sample dashboards), I hope this site may help to contribute to building and maintaining consensus and thus help hasten the delivery of pensions dashboard services for million of working age UK consumers.

Why me?

For many years, I’ve felt personally that if I could see all of my pensions in one place, and come back to this place often (not every day, but certainly a few times a year), then I’d feel much more confident about a) what I’ve already built up and b) my prospects for the future. From research, we know that many, many people in the UK (i.e. millions) feel the same way.

It seems instinctive to me that by being able to easily see the totality of their accumulated pension incomes, people will feel both more aware and more confident of what their pensions might mean for them in their later life. And if their total pension income shown is inadequate, at least they are armed with that knowledge.

But apart from my long-term general interest in this topic, there are three specific reasons why I think I’m quite well-placed to support the pensions dashboards debate:

1. Experience of industry / Government collaboration: Establishing Nest in 2008 broke new ground. None of us involved (whether civil servants or external pensions consultants) had ever before created, in statute, a national trust-based defined contribution pension scheme, with a public service obligation to accept all employers who wished to use it. And all under the glare of close public and media scrutiny.

I would describe the process we adopted to develop the Nest scheme rules as “collaborative innovation”. That is, the pooling of good ideas from a variety of sources, debating and refining them in a spirit of trust and collaboration, and then packaging them appropriately for approval by Ministers, Parliament and other relevant authorities.

A similar spirit of collaboration and trust, across the whole consumer, pensions and technology communities, and Government and regulators, is essential as we bring pensions dashboards to fruition.

2. Of an age where I’m personally thinking about what consumers need: I’m now 58, nine years on from the classic age of 48 where “retirement reality” starts to kick in according to NFU Mutual’s 2013 research.

So I’m personally in a position of thinking about what I would like pensions dashboard services to look like and what I would need them to do.

Plus, many of my friends and peers are of a similar age. Now that our children have grown up and are starting to leave home, pensions issues are increasingly a part of our conversations, helping me gain a deeper understanding of the broader requirements for pensions dashboards (and the fears people have).

(Important note: Pensions dashboards aren’t just for oldies like me, but we know from consistent international evidence that 50-somethings will be the major users, at least initially.)

3. A pensioner since my 40s: I’ve actually been a pensioner since I was 46. My lovely wife Heather very sadly died in June 2014, just before I started this blog.

Heather worked for Prudential, and later as a Teaching Assistant, so was a deferred and active member of two defined benefit (DB) pensions schemes. This meant, when she died in June 2014, I became a spouse pensioner of both the Prudential Staff Pension Scheme and the Berkshire Pension Fund.

So, about 20 years earlier than most people do (because I was only 46), I learned what it feels like to receive a monthly retirement income, guaranteed to pay out until I die, and increasing every year.

This means I already think like a pensioner, with a personal understanding of issues around life expectancy, death, and making the most of your money right up to the day you die, and beyond for your dependents. For more on this, see Episode #6 of 9 in my Dashboards Nine-Nine series of articles in PensionsExpert.

Many thanks for reading this dashboards blog. Please do get in touch if you’d like to discuss any aspect of pensions dashboards (see Contact page for details).

Richard Smith

December 2025