28 April 2026, 5 minute read

This is Part 1 of my new 3-part blog and podcast series about how pensions adequacy is personal.

With the Pensions Commission about to publish its interim report on the whole of UK society’s adequacy, I want to show how pensions adequacy is actually highly personal – across your work, after your death, and through your whole life in between.

For details of the whole series, see my Adequacy page.

The blog is for payroll & pensions professionals but read it as the consumer you also are.

Part 1 – Your pension springs from work

How’s your work life story going?

You’re one of c.42 million working age adults in the UK, each with a unique work life story.

Your unique work life story

Maybe you’ve been in the same job ever since you left school, college or uni. Or maybe you’ve had several different jobs. Maybe you’re full-time, or part-time.

Or maybe you work for yourself, or had a mix of employment and self-employment.

Maybe you’re not in the paid workforce but are doing absolutely essential unpaid work for our society, such as caring for your children, or for adults in your family.

Or maybe, at the moment, you’re doing voluntary work, or not able to work at all.

Whatever your story’s been since you left school, it’s unique to you.

I wanted a graphic to illustrate this, so I asked Claude AI to create one (Claude suggested that each person in the graphic could represent a million real people):

Unprompted, Claude chose to represent the following types of work (it’s not an exhaustive list of all job types, but it’s not a bad spread):

Your unique stack of pensions

(which sprang from your unique work story)

Of course, since 2012, if you’ve earned over a certain threshold amount, your employers’ payroll teams have been required to automatically enrol you into the organisation’s chosen pension scheme.

You might also be lucky enough to have pensions from before 2012 (not everyone does).

If you’ve had periods of self-employment, you might’ve set up a personal pension. Or you might’ve brought together previous workplace pensions.

Because your work life story is unique, so is the random “stack” of different pensions which you’ve built up through your different (self-)employments.

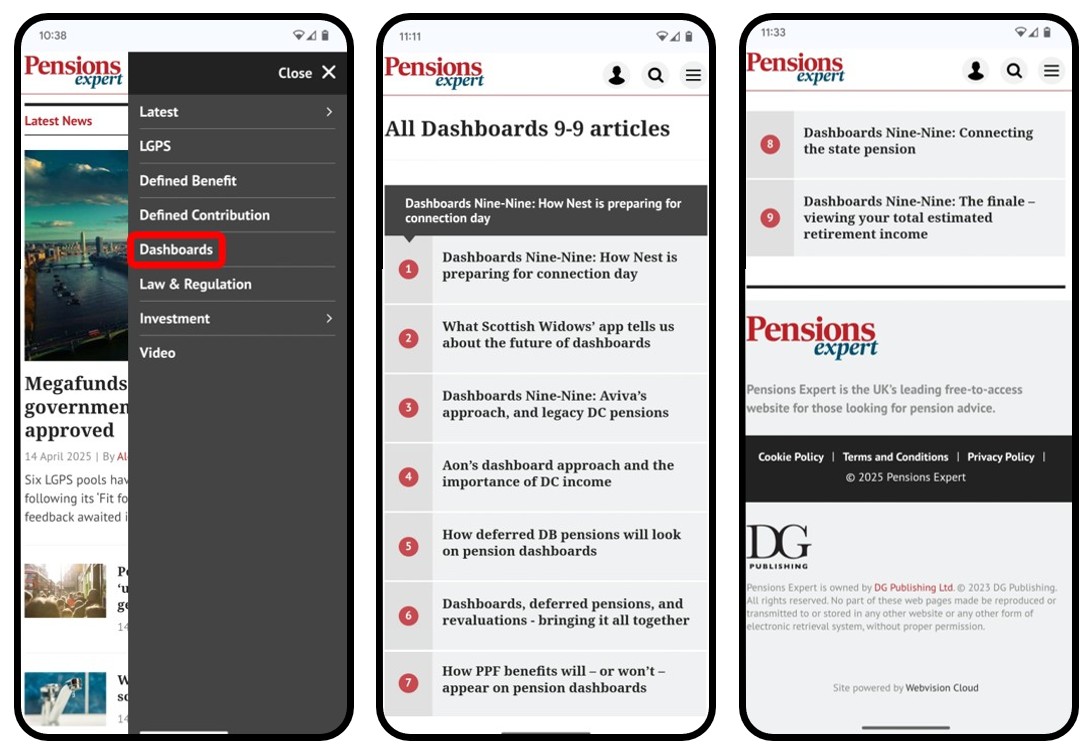

Example: To illustrate this, in 2024-25, I wrote about my own unique work story and pensions in a series of articles in Pensions Expert – Dashboards Nine-Nine:

In summary, working backwards from 2025 (when I turned 58 and “semi-retired”) right back to 1987 (when I was 20), my career has comprised employments with:

Umbrella employer Parasol, PricewaterhouseCoopers, Aon, The Automobile Association (AA), Prudential (now M&G) and the CE Heath Group (now part of Capita).

I bet you too could easily list all your different employers, right?

However, would you also be able to so easily list all the different pensions which those different jobs have generated?

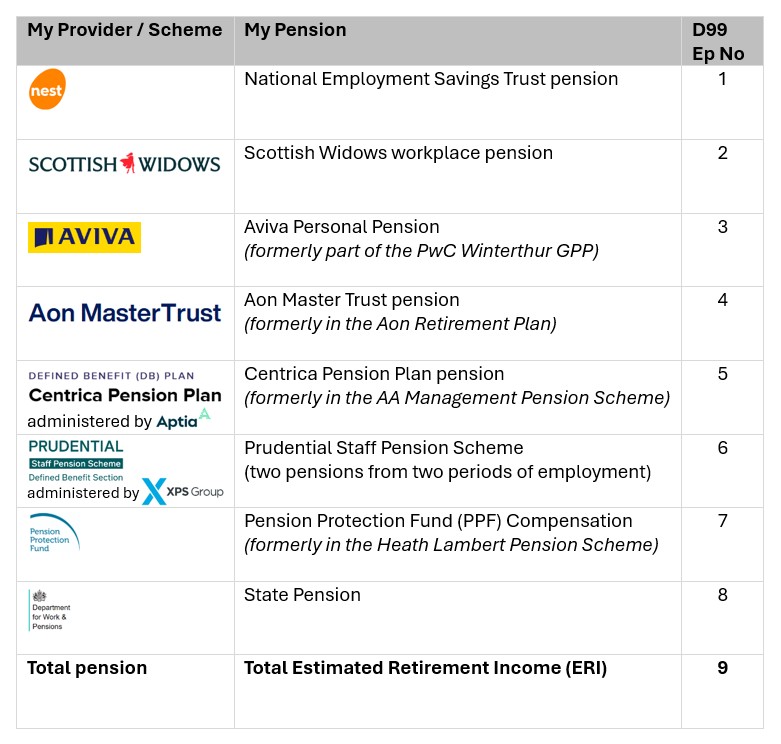

Here’s my unique “stack” of pensions derived from my unique work life story (also showing how the pension names have changed over time, for various reasons):

If you can list your unique stack of pensions, then you’re in the minority.

Most of the UK’s c.42m working age people don’t know:

a) all the pensions they’ve built up, let alone …

b) what income in retirement each pension might provide, and certainly not …

c) whether, in aggregate, that’ll be enough (or “adequate”) for them to live on in their later lives.

It’s a big issue for UK society. Which the government is addressing…

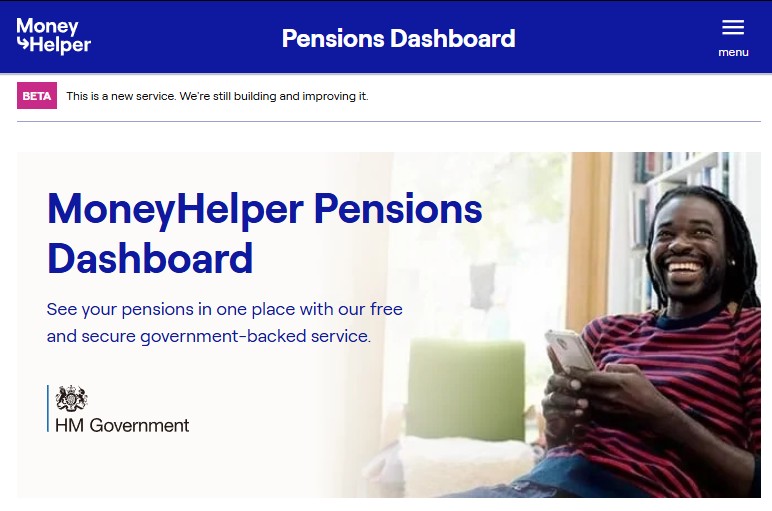

Studying what you might get

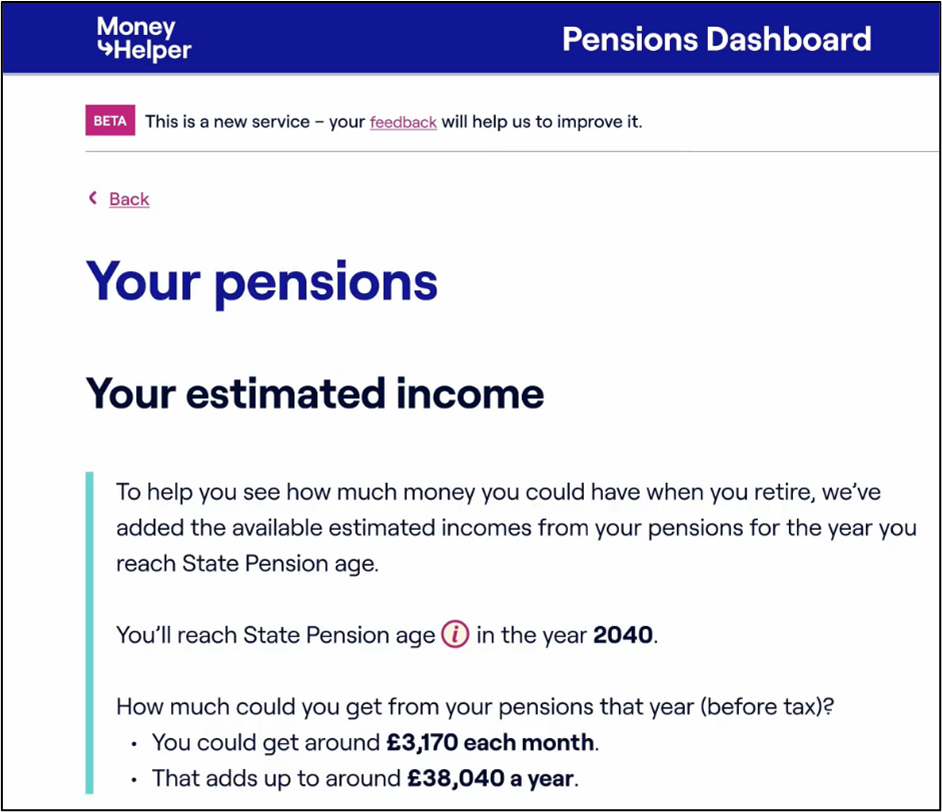

… by developing the secure online MoneyHelper Pensions Dashboard (MHPD) service:

For the first time in the UK, the MHPD enables ordinary citizens to see and study their own unique stack of pensions, built up across their unique working life.

Crucially, at the top of the main MHPD summary page, users can see what Total Estimated Retirement Income (ERI) they might get from their State Pension age, totalled across all their different pensions:

Seeing this monthly total ERI enables people to consider their own personal pension adequacy, asking:

“Will that total monthly income be enough, or ‘adequate’, for the life I want after work?”

(See my ERICA page – Estimated Retirement Income Check for Adequacy for more thinking on this)

Today, most people never ask this adequacy question.

Not because they don’t care – indeed, many are very concerned about it.

But because the system has made it very difficult to study what your monthly total ERI might be and to consider whether it might be enough for your unique needs in later life.

The MHPD changes all that. It finally ends the invisibility of (in)adequacy.

That’s because to properly study whether your total ERI is adequate for your needs means looking at the unique stack of pensions you’ve built up so far (plus assumed future contributions) – that stack having sprung from your unique work life story to date.

This is what the MHPD enables.

But what if a user feels the total ERI they see on the MHPD won’t be enough to live on?

This is something I discussed on the latest episode of ‘Behind the Button’ – the podcast from The Chartered Institute of Payroll Professionals (CIPP):

As I said on the pod, one thing people might be prompted to think is:

“Could I increase the pension contributions going in today to make my Total ERI bigger?”

This could lead to “upstream” worker conversations with employers and payroll, especially about any employer contribution matching which hasn’t been taken up.

In 2022, research from Nest Insight found employers report 38% of workers eligible for employer matching don’t take up the full match, meaning many people are leaving money on the table that could be helping them move more towards a total income that would be “adequate” for them.

The opportunity is to reframe this as more value for the workforce, not just more cost.

So payroll teams need to prepare. Are you ready for those conversations with staff? And, for those staff who want to act, how low-friction is your contribution-increase process?

Summary

Pensions spring from work, but work life stories are unique, meaning adequacy is a personal issue.

Adequacy is a relationship between your unique past to date and the choices you make today for your future. Good choices start with visibility:

- Study: seeing your total ERI on the MHPD, then really thinking about whether that monthly income will be adequate for the later life you want, built up from …

- Stack: your unique collection of different pensions, listed together simply and securely for the first time on the MHPD, which themselves have sprung from …

- Story: your unique work life story, so far, across your different employments.

Payroll teams need to prepare to smoothly support those workers who wish to increase contributions, including take up of any unused employer matching.

In Part 2 of this blog and podcast series, I’ll broaden this personal adequacy thinking about what income your loved ones might need after you’re gone, including speaking with the lovely Claire 7 Chris Sandys on The Silent Why podcast.

And Part 3 will think about the need to spread your spending consumption over the whole of your life.

Thanks so much for reading to the end.

RS, 28.4.26